Social Security’s Fiscal Clock Is Running Out — And Washington Won’t Look At It

The math on Social Security has been broken for years. The fixes exist, the trustees publish the numbers annually, and Congress keeps changing the subject.

Typically, our afternoon content is reserved for our paid subscribers or exclusive to those of you who financially support this effort. This one is open to all.

You can subscribe for FREE to get most of our content delivered to your inbox. A PAID subscription is $7 a month or $70 a year, and it gets you access to ALL of my stuff (like this full column). Why subscribe? Because now more than ever, you need someone calling balls and strikes, and who isn’t owned by interest groups.

Because of the chart-heavy nature of this column, it is not available on our podcast channel.

🕐 4 min read

The Bargain That Actually Penciled Out

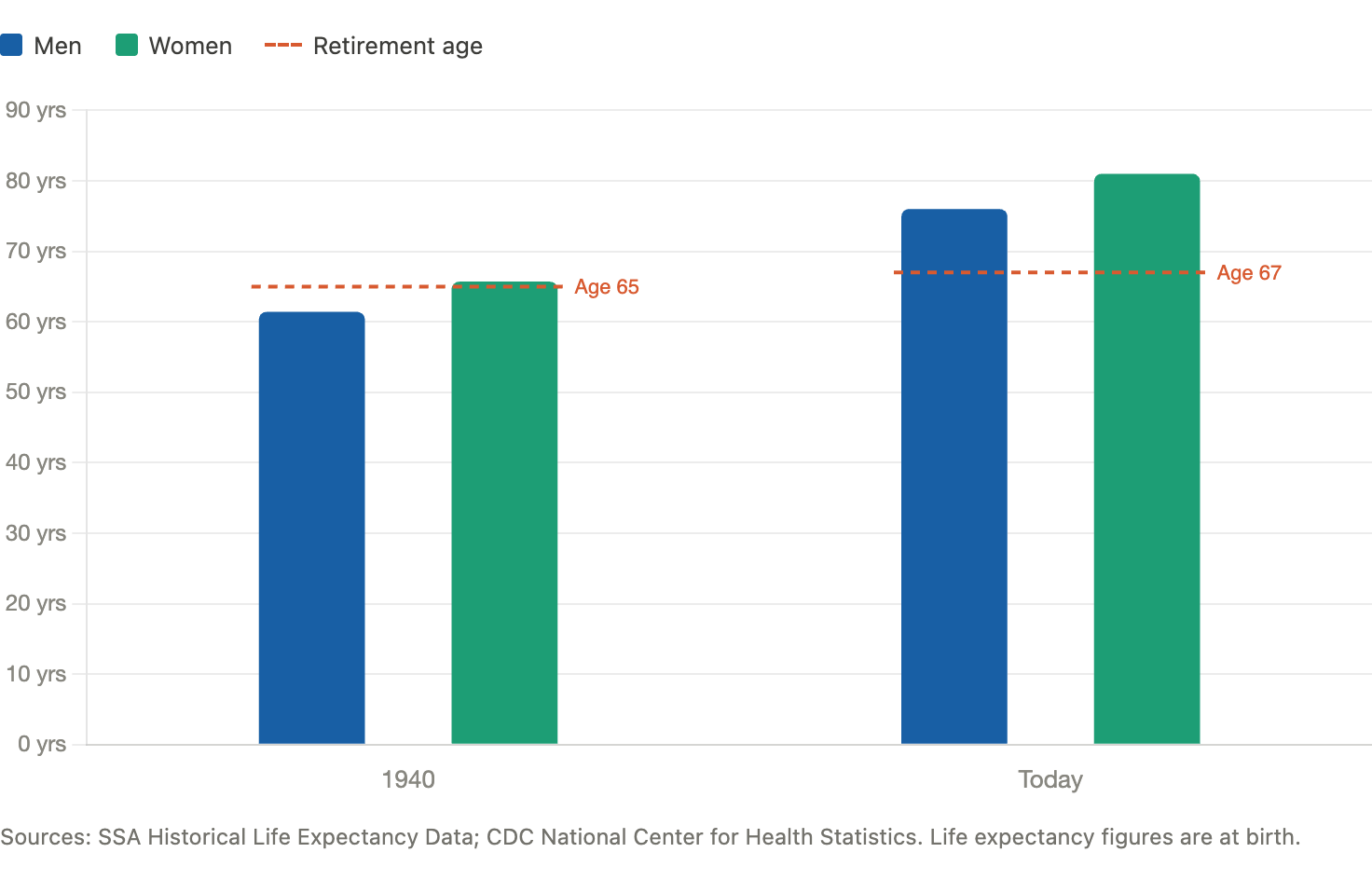

When Ida May Fuller received the first Social Security check in January 1940 — $22.54 — the program looked like a reasonable bargain. She had paid into the system for three years. Life expectancy for American men at the time was 61 years. The retirement age was 65. The math, while not generous, was at least coherent.

It isn’t anymore.

Today, American men live to 76 on average. Women live to 81. The retirement age has crept up by just two years — to 67 — while life expectancies have grown by fifteen. The deal that launched Social Security has quietly, steadily come apart, and almost nobody in a position to fix it is willing to say so.

The Numbers They Publish Every Year

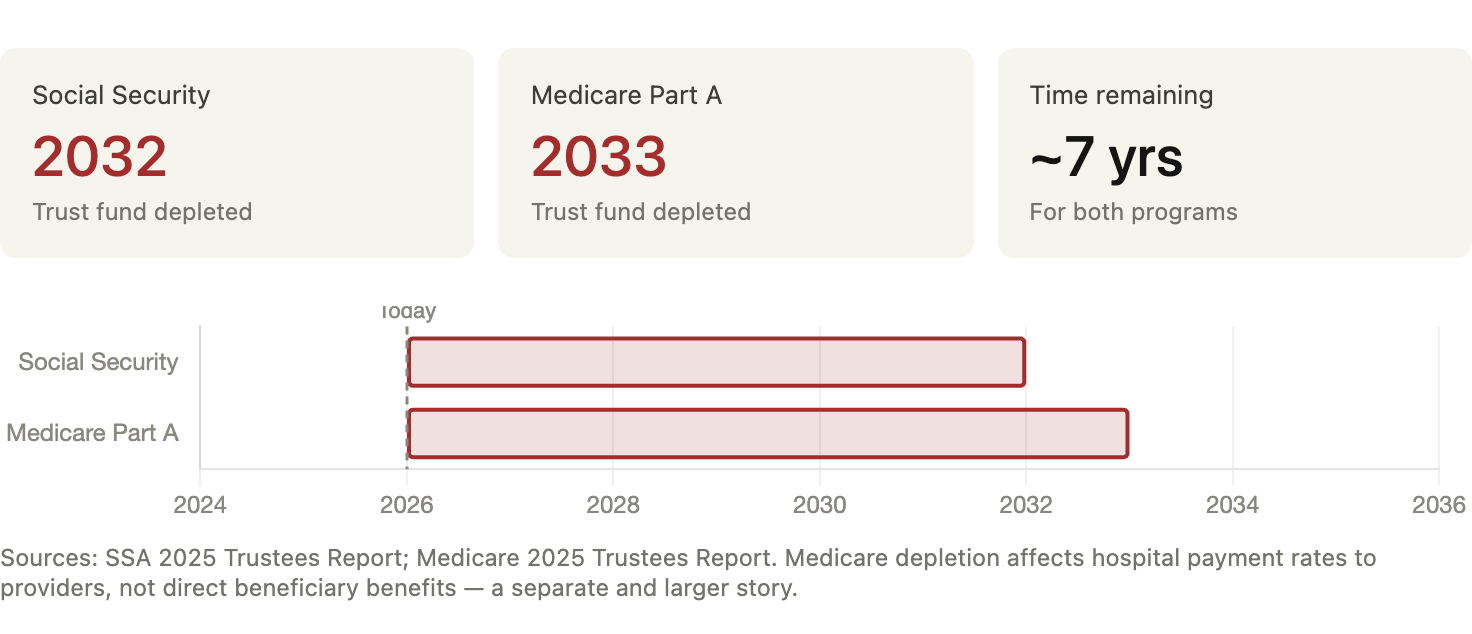

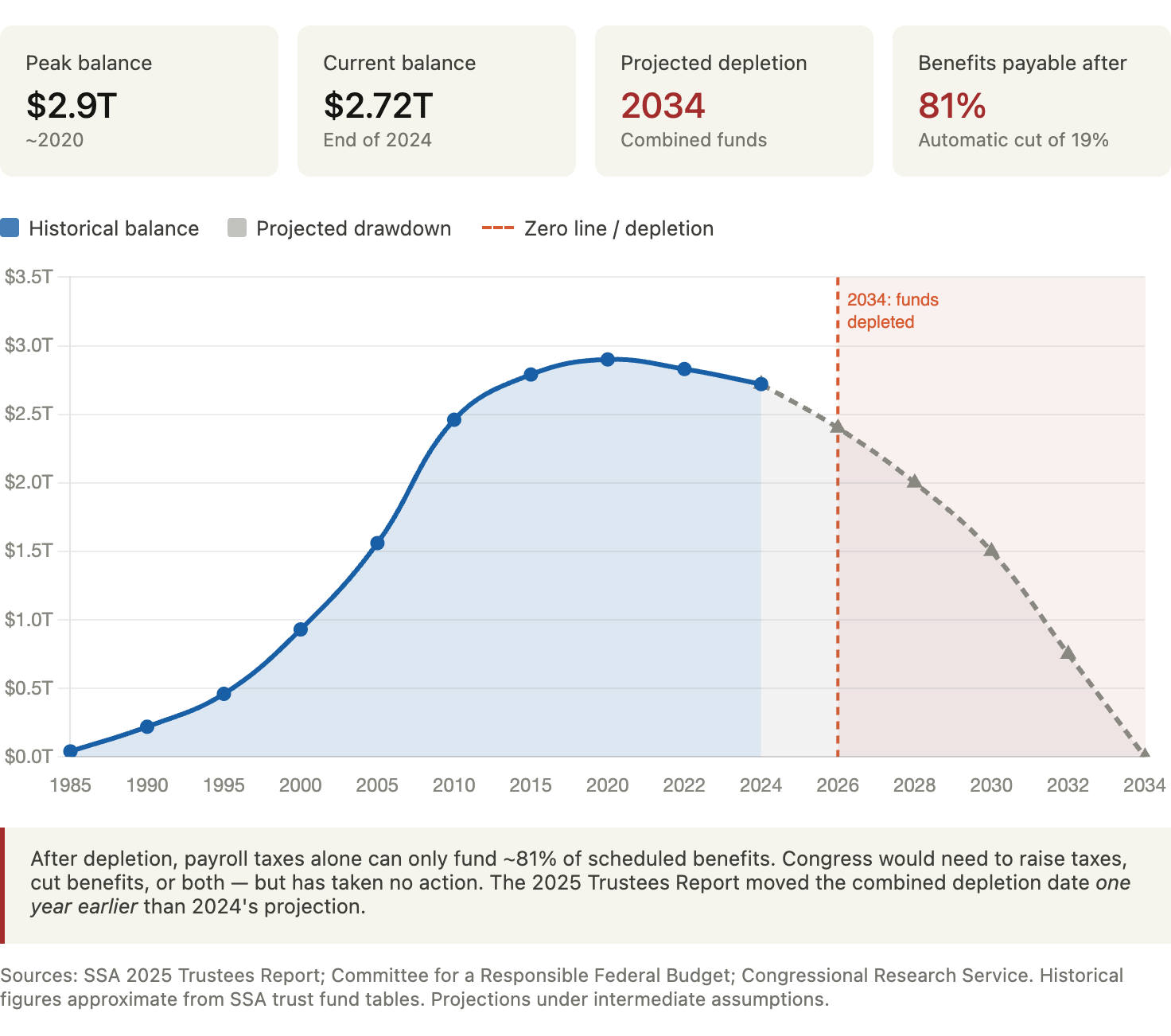

The Social Security Trustees release an annual report on the program’s financial condition. This June, their 2025 edition delivered the latest update: the combined trust fund will be depleted by 2034 — one year sooner than last year’s projection. At that point, with the reserves gone, payroll taxes alone can fund only 81 percent of scheduled benefits. That means an automatic, across-the-board cut of 19 percent — roughly $376 less per month for the average retiree — unless Congress acts before the clock runs out.

Congress has not acted.

The trust fund surplus that papered over the gap for four decades peaked near $2.9 trillion around 2020. It is now draining at $67 billion a year and accelerating. The program isn’t hiding its condition. The problem is that nobody in Washington finds it politically convenient to read the report out loud.

A Pyramid That’s Flipping Upside Down

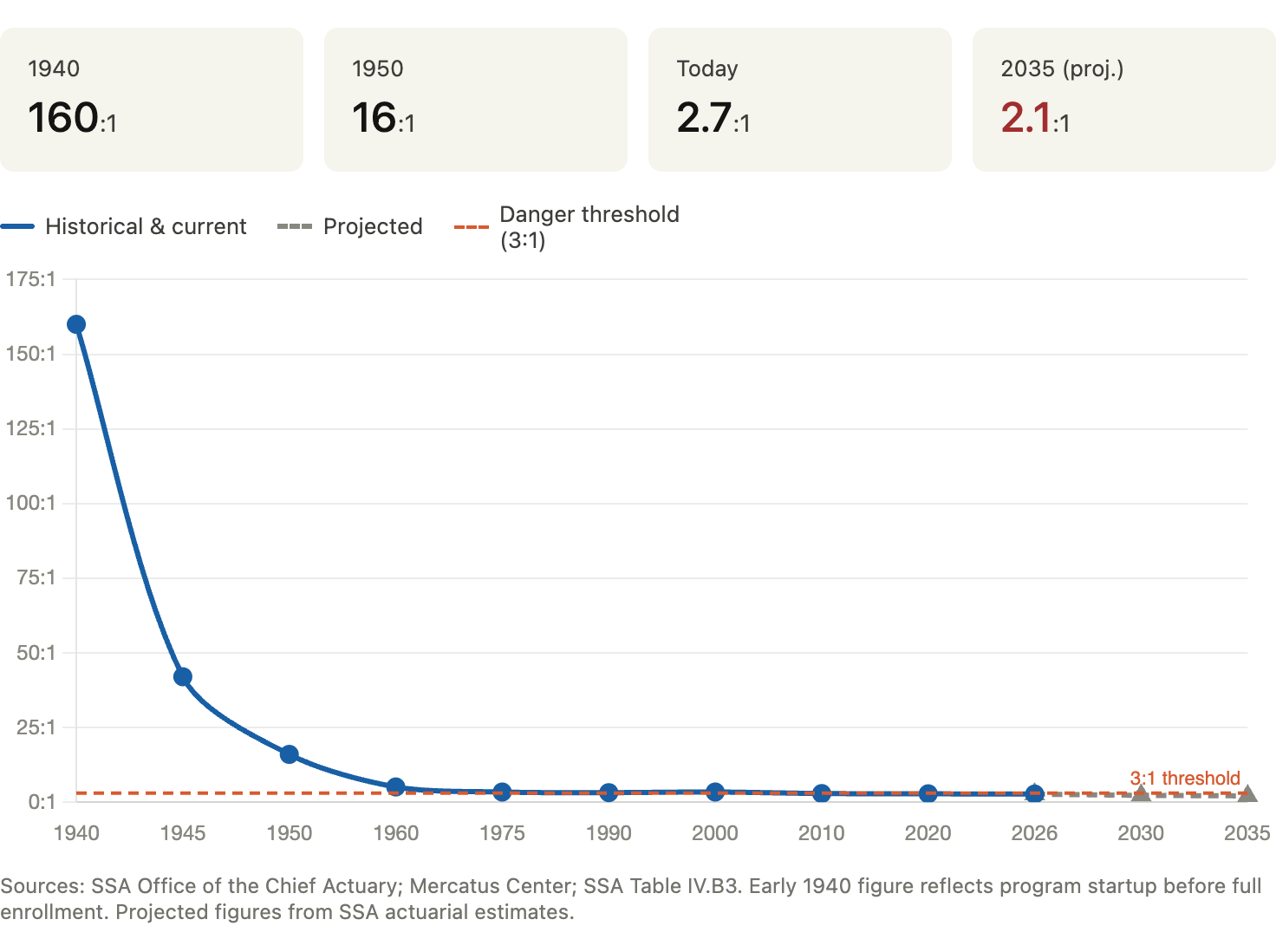

The structure of Social Security has always been pay-as-you-go — current workers fund current retirees, with no individual savings account, no invested capital, no actuarial cushion beyond the trust fund itself. That arrangement works tolerably well when the worker base is large and growing. It works very poorly when the demographic pyramid inverts.

In 1940, there were 160 workers for every retiree. Today, there are fewer than 3. By 2030, that ratio is projected to fall to 2-to-1. Birth rates have fallen, the Baby Boom generation is in full retirement, and the math that once held this system together has quietly stopped working. What happens after 2034 if nothing changes? The program doesn’t disappear — payroll taxes keep coming in and keep paying benefits, just not all of them. The Trustees project that by 2099, payroll revenue will cover only 72 cents on every dollar of promised benefits.

That may be the most politically dangerous feature of this crisis. It is slow enough that no single moment forces a reckoning.

The Fixes Exist. That’s The Problem.

The solutions are not mysterious. Raise the payroll tax rate. Lift or eliminate the income cap — currently $184,500 — above which earnings aren’t taxed. Raise the retirement age to reflect actual life expectancies. Means-test benefits so that the wealthy receive less. Analysts across the ideological spectrum have run the numbers, and the arithmetic closes.

What doesn’t close is the political will.

Every one of these fixes requires asking someone to pay more or receive less, and in Washington, that conversation tends to end careers. What makes the current moment particularly uncomfortable is that the easy off-ramp is gone. The Congressional Budget Office is unambiguous: because lawmakers have waited so long, no single lever is sufficient anymore. It now takes a combination of painful changes, phased in over time, to restore solvency — and every year of inaction makes that combination more painful and shortens the timeline. The Republican budget bill passed in July prompted Social Security’s own actuaries to move the depletion date up to 2032. So there’s that.

So, Does It Matter?

Workers in their twenties and thirties today are paying full payroll taxes into a system that, under current projections, will pay them back somewhere between 72 and 81 cents on the dollar at retirement. Ida May Fuller, that first beneficiary, lived to 100 and collected $22,888 in lifetime benefits on $24.75 in contributions. Nobody begrudges her that. The program was designed to be there when people needed it.

The clock is running. The math is public. The fixes exist. What’s missing is the willingness to say any of this out loud in a place where it might actually matter.

If you want to entertain yourself, you could reach out to a Member of Congress - your own or another- and ask them what they are doing to confront and deal with this problem. And, yeah, if this isn’t enough of a problem, don’t ask about the solvency of Medicare.

Here’s a chart on that…