California’s Billionaire Wealth-Taking Plan: Crossing The Line Between Taxation And Confiscation

A One-Time Wealth Levy That Moves California From Taxing Income To Charging For What People Own

Our morning content is for all of our subscribers and site visitors. If you like this kind of content, please consider a paid subscription! You can listen to this content on your favorite podcasting app - just search for So Does It Matter: Spoken. Or go here.

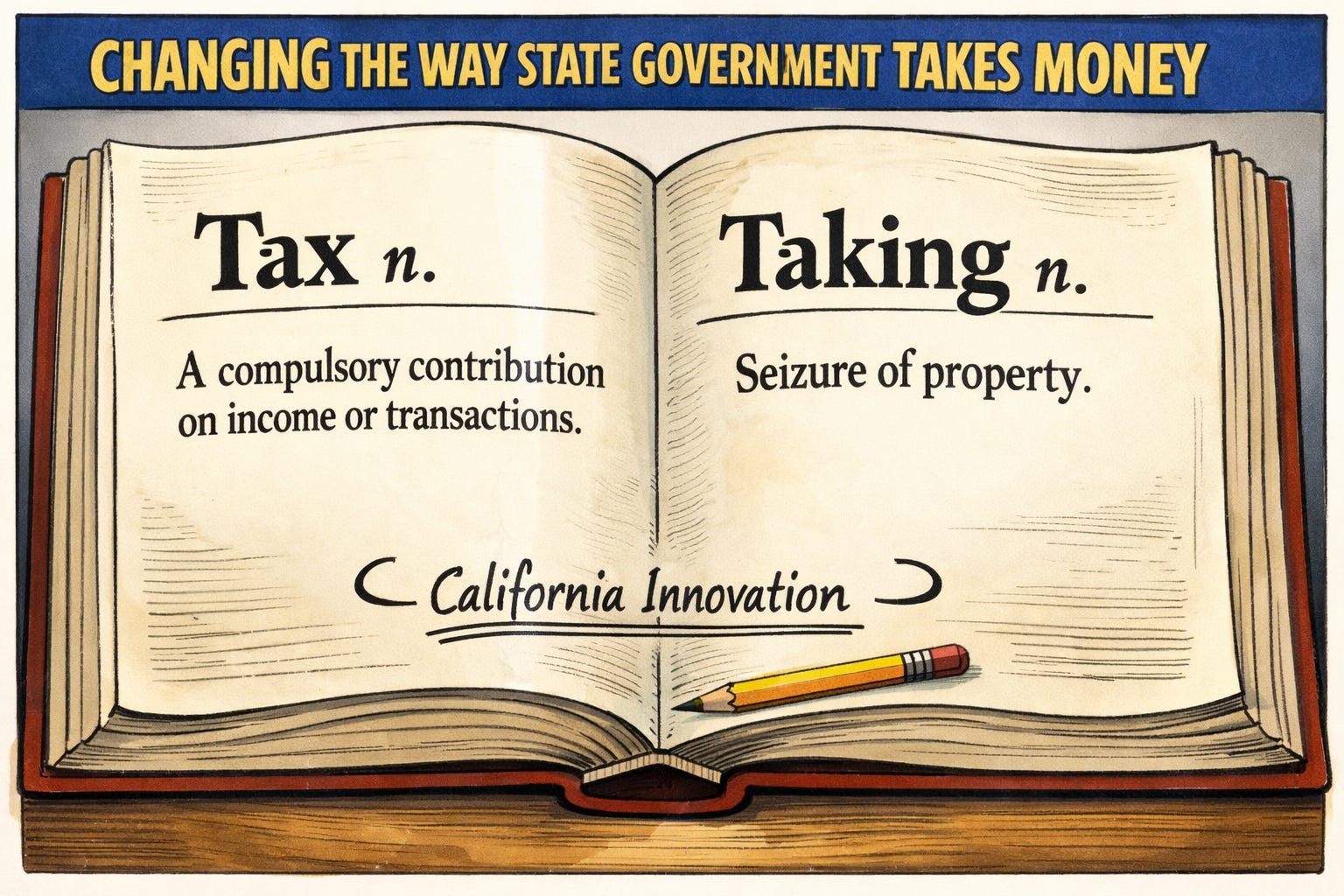

We will be writing a lot about this proposed “net-worth taking” of California’s billionaires. There’s a lot to not like about it. But first, we have to deal with the big lie: this is not a tax, it’s a taking.

Below the paywall are three runner-up cartoons that almost made it up top! All worth checking out.

⏱️ 6 min read

The Wealth Snapshot

Imagine sitting down to file your California income tax return and discovering that the state wants something new from you — not just what you earned, but what you own. Your home, your investments, your business interests, your real estate, your personal property.

That is the shift embedded in an initiative measure being promoted by one of California’s largest public employee unions — a proposed one-time wealth levy. It is sold as a 5% tax on individuals with a net worth above a billion dollars, pitched as a tidy answer to budget pressure. It replaces a tax system based on what you earn with one based on what the state says you own, and that is the line between taxation and confiscation.

This is not an adjustment to income tax rates or a tweak to capital gains. It is a move from taxing annual earnings to taxing the accumulated property a person has built over a lifetime.

From Flow To Holdings

For decades, California has taxed economic activity. Income is taxed when it is earned, purchases are taxed when they are made, and property is taxed on an annual basis. The focus has been on activity — money coming in, transactions occurring, assets held year to year under defined rules.

The one-time wealth levy breaks from that structure. It takes a snapshot of accumulated holdings on a fixed valuation date and applies a percentage charge to the whole. That includes business interests, partnership stakes, intellectual property, investment portfolios, and other assets that often have no simple cash value.

To execute that plan, the state must define net worth, impose valuation standards, require disclosures, and empower auditors to challenge asset estimates. Private companies must be valued without a public trading price, and assets tied up in long-term ventures must be assigned numbers that withstand scrutiny.

If wealth is liquid, a check can be written. If it is tied up in a company or long-term investment, assets must be sold, borrowed against, or diluted to generate cash.

“I don’t have the liquidity” is not an answer the state accepts.

Targeted And Backward-Looking

Three features push this beyond ordinary taxation.

First, it is, in effect, backward-looking: it imposes a bill based on wealth built long before the levy was proposed.

Second, it is described as nonrecurring — a one-time charge justified by fiscal pressure.

Third, it targets a tiny class defined by a statutory threshold of $1 billion.

That narrow targeting is what makes the measure politically viable. When a tax affects only a couple of hundred people, it can be framed as painless and overdue.

The difficult step is not lowering the threshold. It establishes the principle that accumulated net worth is a legitimate target for one-time extraction. Once that principle is accepted, the number attached to it becomes a matter of politics.

The selling point is that it is small, targeted, and supposedly temporary, which is precisely what makes the precedent so consequential.

The Administrative Machine

Taxing wealth requires building machinery to measure wealth. That means reporting requirements, valuation formulas, certified appraisals, and expanded audit authority to examine private enterprises and complex trusts.

Consider a privately held business. The owner must assign a fair market value without a public trading price, defend that number in writing, and defend it again under audit. When the state can demand that process for a single bill, it has created a wealth-reporting regime, not merely a tax.

Once that infrastructure exists, it does not disappear. Bureaucracies grow around it, and enforcement authority expands through regulation and interpretation.

Today, the threshold is $1 billion. Tomorrow, it becomes whatever number a future Legislature determines will generate revenue.

Already Taxed Once

Wealth is built from income, investment gains, and asset appreciation, all of which are already taxed under California law.

High earners face marginal income tax rates above 13 percent, and capital gains are taxed at ordinary income rates. Property is assessed annually, and consumption is taxed at the register.

A five percent levy on net worth adds another layer on top of that structure. It does not tax new economic activity; it taxes what remains after prior taxation.

Calling that fairness does not alter its character.

The Risk Beyond The Threshold

Many Californians will dismiss this as someone else’s problem. Perhaps that reaction is part of the design.

In California, “one-time” revenue ideas rarely remain one-time in political expectation, even when the statute says otherwise.

Once a state crosses the line from taxing income to taxing accumulated wealth through a one-time levy, the precedent is set. The administrative framework exists, and the argument has been normalized. Political thresholds tend to move when deficits persist.

So, Does It Matter?

Governments rarely surrender revenue tools once they acquire them.

When fiscal pressure intensifies, lawmakers use whatever mechanism is available. A wealth levy aimed at billionaires may feel politically painless today, but the principle it establishes extends far beyond the number attached to it.

The shift from taxing what people earn to taxing what they own reflects a view of state authority that reaches into accumulated property itself. Once the state builds a system to price that property for taxation, it will not forget how to use it.

SOMETHING EXTRA FOR OUR PAID SUBSCRIBERS - THREE BONUS CARTOONS. ALL FAIRLY ALARMING… JUST BELOW THE PAYWALL.