America’s Debt Crisis May Be Far Worse Than Washington Admits

One of the nation’s leading budget experts argues that even Washington’s frightening debt projections may dramatically understate the fiscal challenges ahead.

Typically, our afternoon content is either reserved for our paid subscribers or exclusive to those of you who financially support this effort. Often on Friday afternoons, we lift the paywall, like today! Enjoy!

You can subscribe for FREE to get most of our content delivered to your inbox. A PAID subscription is $7 a month or $70 a year, and it gets you access to ALL of my stuff (like this full column). Why subscribe? Because now more than ever, you need someone calling balls and strikes, and who isn’t owned by interest groups.

You can also listen to this post on our podcast feed, So, Does It Matter? SPOKEN. It is available on your favorite podcast app. And here.

🕒 5 min read

The Debt Clock Keeps Spinning

America’s gross national debt has now climbed past $39 trillion, a figure so large that most of us have long since lost the ability to truly comprehend it.

Over the past year alone, the debt increased by nearly $3 trillion — an average of more than $8 billion per day. Despite endless campaign promises about fiscal responsibility, neither political party has shown much willingness to confront the problem seriously.

Republicans campaign on spending restraint and too often abandon it when handed power. Democrats continue to demand new spending while showing little serious interest in reforming the entitlement programs driving the long-term crisis. The result is a debt trajectory that continues to worsen regardless of which party controls Washington.

The official projections are already alarming. According to the Congressional Budget Office, federal debt held by the public is expected to climb from roughly 100 percent of GDP today to about 175 percent by 2056.

That should be enough to command the attention of every policymaker in America.

But according to one of the nation’s most respected budget experts, even those frightening projections may be far too optimistic.

A Baseline Built On Fantasy

Jessica Riedl of the Brookings Institution has now provided a sobering follow-up to her recently released Spending, Taxes, and Deficits: A Book of Charts, which I wrote about recently right here (a ‘must-read’). Her new analysis focuses on a deceptively simple question: what if Washington’s already alarming debt projections are still too optimistic?

Riedl is not some fringe commentator making sensational predictions. She is widely regarded as one of Washington’s foremost experts on federal budgeting and fiscal policy. Her warning is not that the debt outlook is bad. Her warning is that the numbers most people cite may substantially understate just how bad it is.

The issue lies in how the Congressional Budget Office is required to construct its long-term projections. By law, CBO generally projects future spending and revenue based on current law rather than on what Congress is actually likely to do.

That may sound reasonable. In practice, it can produce assumptions that many observers view as unrealistic.

The baseline assumes temporary tax cuts expire, federal spending shrinks significantly as a share of the economy, smaller entitlement programs are constrained, and current tariff policies remain in place indefinitely. Those assumptions may satisfy budget rules, but they do not accurately reflect the behavior Congress has demonstrated over many years.

“The federal debt outlook is $62 trillion worse than is commonly reported.”

That is the central warning of her analysis.

The Real Numbers May Be Much Higher

Riedl’s research attempts to estimate what happens if Washington largely continues its current habits rather than following the assumptions embedded in the official baseline.

The results are sobering.

Instead of debt rising to approximately 175 percent of GDP by 2056, it could reach roughly 243 percent. In practical terms, projected federal borrowing over the next three decades increases from about $138 trillion to approximately $200 trillion.

That is an additional $62 trillion in borrowing beyond what is commonly reported.

To put that in perspective, $62 trillion is larger than the entire annual economic output of the United States today.

What makes the analysis particularly troubling is that it does not rely on a catastrophic recession, a military conflict, or an unforeseen national emergency. It is largely based on the assumption that Washington will continue to do what it has repeatedly done: extend temporary policies, avoid politically painful spending reductions, and postpone difficult fiscal decisions.

In other words, the risk comes not from a crisis. The risk comes from business as usual.

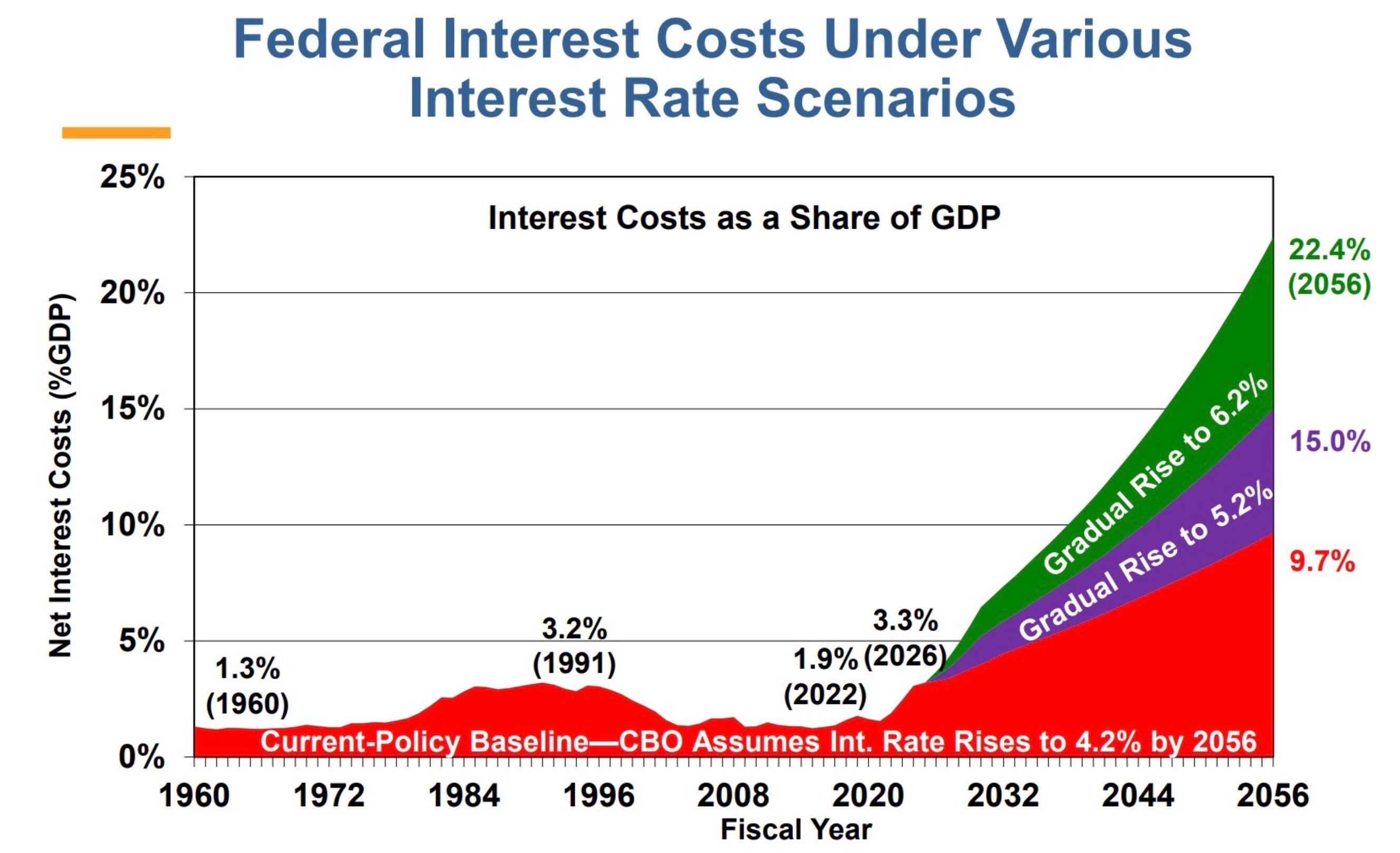

The Interest Rate Trap

There is another major vulnerability lurking beneath the surface.

The Congressional Budget Office assumes that despite this mountain of federal borrowing, average interest rates on government debt remain relatively manageable over the coming decades. Specifically, the long-term projections assume rates remain around 4.2 percent.

That assumption matters enormously because interest costs compound rapidly as debt accumulates.

If rates were just one percentage point higher — 5.2 percent rather than 4.2 percent — the debt picture worsens dramatically. Under that scenario, debt levels could exceed 300 percent of GDP by 2056.

A seemingly modest increase in interest rates would add roughly $57 trillion more to the debt burden.

At that point, the federal government risks entering a vicious cycle in which borrowing drives up interest costs, which then require even more borrowing to cover them.

The debt itself becomes one of the government’s largest and fastest-growing expenses.

So, Does It Matter?

One can certainly debate the assumptions in Riedl’s analysis. Long-term economic forecasting is inherently uncertain, and no one can predict the next 30 years with precision.

But her broader point is difficult to dismiss.

Washington’s official debt projections are already alarming. If those projections depend on policy changes that Congress is unlikely to make, then the nation’s fiscal outlook may be considerably worse than most Americans realize.

For decades, elected officials in both parties have found it easier to promise benefits than to pay for them. The bill for those decisions continues to grow.

The most unsettling aspect of Riedl’s warning is not that America faces a debt problem. Most Americans already know that.

It is that even the scary numbers may be understating the scale of the crisis.

If Washington will not make hard decisions when the debt is $39 trillion, why should anyone believe it will suddenly find discipline when the number is $50 trillion, $75 trillion, or $100 trillion?

That is the real warning here. The debt crisis is not just approaching. Washington is already choosing it.

Ask your Member of Congress. Ask your United States Senator. Ask your President.

What are you doing about this?